Apply for Council Tax Reduction

Changes from 1 April 2026

We're introducing a new income banded Council Tax Reduction (CTR) scheme for working age applicants.

The aim of the new scheme is to make the amount of support customers receive more stable month-to-month. The scheme also offers those on the lowest incomes up to 100% discount on their council tax bill.

You may get a discount of:

- 100%

- 75%

- 50%

- 25%

- 0%

This depends on who's in your household and which band your income falls into.

If you're pension age, you will continue to be assessed under the national Council Tax Reduction Prescribed Scheme and can receive up to 100%.

Who can apply

You can apply if you:

- are liable to pay Council Tax

- are on a low income

- have capital below £6,000 for working age claims

- have capital below £16,000 for pension age claims (or are in receipt of Pension Guarantee Credit)

How to apply

Apply online by completing the application form.

If you do not provide the evidence within 21 days of submitting the form, your claim will be refused and you will need to reapply.

If you've already started a claim online, you can retrieve a claim that you have already started.

If you need support completing your application, contact our Customer Services Team.

Under the national scheme, your council tax bill could be reduced by up to 100% depending on your circumstances.

The amount of Council Tax Reduction you receive will depend on:

- your income, including any benefits

- your savings

- your household size

We can also assess your entitlement for Alternative Maximum Council Tax Reduction (Second Adult Rebate). This is a reduction in your council tax if you have a low-income second adult living with you who:

- is 18 or over

- is not your partner

- is on a low income or gets certain benefits

- does not have joint responsibility with you for paying council tax

You must apply for the reduction rather than the second adult.

How much 'second adult rebate' you will get

If the second adult in your home is getting one of the following benefits, you will get a 25% reduction on your eligible council tax:

- Income Support

- Pension Credit

- Job Seekers Allowance (income based)

- Employment and Support Allowance (income related)

If the second adult is not on one of the benefits listed above, the table below shows the percentage reduction:

| Combined gross income of second adults (from 1 April 2026) | Reduction applied |

|---|---|

| Less than £289 per week | 15% reduction |

| £276 to £374.99 per week | 7.5% reduction |

| £375 or more per week | No reduction (Nil) |

Gross income is not only from employment (for example, the total earnings before tax and National Insurance). It includes income from other sources too.

Your weekly income is compared to the income bands for your household type.

Your discount is then applied at one of five levels:

- Band 1 - 100% discount

- Band 2 - 75% discount

- Band 3 - 50% discount

- Band 4 - 25% discount

- Band 5 - No discount

If you (or your partner) receive Income Support, Employment Support Allowance (Income Related) or Jobseekers Allowance (Income Based), your claim will automatically be placed in Band 1 (100%).

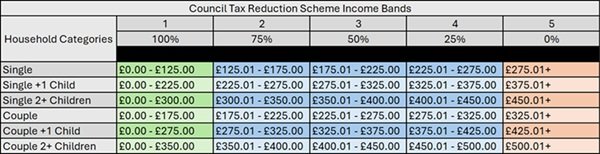

Net income will be applied in the income bands shown in this image (also available in the table below).

{kind=link}

Your net income is the amount of money you receive after any deductions.

| Household category and discount |

1 (100%) |

2 (75%) |

3 (50%) |

4 (25%) |

5 (0%) |

|---|---|---|---|---|---|

| Single | £0 to £125 | £125.01 to £175 | £175.01 to £225 | £225.01 to £275 | £275.01+ |

| Single and 1 child | £0 to £225 | £225.01 to £275 | £275.01 to £325 | £325.01 to £375 | £375.01+ |

| Single and 2 or more children | £0 to £300 | £300.01 to £350 | £350.01 to £400 | £400.01 to £450 | £450.01+ |

| Couple | £0 to £175 | £175.01 to £225 | £225.01 to £275 | £275.01 to £325 | £325.01+ |

| Couple and 1 child | £0 to £275 | £275.01 to £325 | £325.01 to £375 | £375.01 to £425 | £425.01+ |

| Couple and 2 or more children | £0 to £350 | £350.01 to £400 | £400.01 to £450 | £450.01 to £500 | £500.01+ |

When we calculate your income to work out your band, we will disregard the following (this means we will not include):

- Child Benefit

- Child Maintenance

- Carers Allowance

- Attendance Allowance

- Personal Independence Payments

- Disability Living Allowance

- Employment and Support Allowance Support Component

- Armed Forces Independence Payments

- Universal Credit Carer Element

- Universal Credit Disabled Child Element

- Universal Credit Limited Capability for Work and the Limited Capability for Work Related Activity Element

- Universal Credit Housing Element

- War Pensions

- War Disablement Pensions

- Housing Benefit

Additional disregarded income

If you're working, you will receive a £25 disregard from your earned income (per household).

If you claim a disability benefit you will receive a £50 disregard from your income (per household).

We are not disregarding the Transitional Protection element of Universal Credit when assessing income for Council Tax Reduction (CTR) from 1 April 2026. Under the Income‑Banded CTR Scheme, awards are no longer based on an applicable amount. Instead, entitlement is calculated solely on total household income.

Households receiving disability‑related benefits will have an extra £50 income disregard under the Income‑Banded Council Tax Reduction (CTR) Scheme. Disability benefits are intended to help with additional care and living needs, so this higher disregard ensures that support is protected and properly recognised when we calculate CTR entitlement.

If you have £6,000 or more and are working age, you cannot receive CTR.

If you are of pension age, the usual capital limit is £16,000. However, if you receive Pension Guarantee Credit, this limit does not apply because your claim is assessed under national rules.

A non-dependant is someone aged 18 or over (other than a partner) who lives with you. A non-dependant could be a parent, adult son or daughter, relative or friend.

There will be a £5 per week reduction in your discount for each non-dependant that lives with you.

We will not make a non-dependant deduction if you or your partner:

- receive Attendance Allowance

- receive the care component of Disability Living Allowance

- receive the daily living component of Personal Independence Payments

- receive Armed Forces Independence Payments

- are blind or treated as blind

We will also not take a deduction where one of the following applies to the non-dependant:

- they're in receipt of Income Support, Jobseekers Allowance (IB), Employment Support Allowance (IR), Universal Credit with no earnings, or Pension Credits

- they are a member of the armed forces and is away on operations

- they are disregarded under Council Tax legislation (for example, they're a full-time student)

To help households move onto the new scheme, Transitional Relief will be provided for anyone receiving Council Tax Reduction (CTR) when the new scheme starts on 1 April 2026 and whose weekly loss is more than £10.

You will receive Transitional Relief if:

- you are receiving CTR on the date the scheme changes

- you have capital of £6,000 or less, and

- your weekly loss under the new scheme is more than £10

(Households with a weekly loss of £10 or less will not receive Transitional Relief).

Transitional Relief will:

- reduce larger losses when you move to the new scheme

- be paid automatically (you do not need to apply)

- reduce each year as follows:

- year 1: 100% of the calculated Transitional Relief

- year 2: 50% of the Year 1 Transitional Relief amount

- year 3: no Transitional Relief

Transitional Relief will be paid as a single amount on 1 April to eligible households.

This payment helps cover part of the difference between your CTR Award on 31 March 2026 and what you receive under the new scheme.

Transitional Relief only applies if your weekly loss is more than £10 and is calculated as follows:

- Weekly loss between £10.01 and £15, Transitional Relief will cover 50% of the amount above £10, up to a maximum of £2.50 per week.

- Weekly loss more than £15, Transitional Relief will equal:

- £2.50 (50% of the first £5 above £10), plus

- 100% of any loss above £15

This means no household will lose more than £12.50 a week (£651.79 a year); for example, if the loss is £20 per week, Transitional Relief would reduce it by £7.50 bringing the loss down to £12.50 per week.

Transitional Relief is temporary. It is designed to ease the transition, not remove all differences between the old and new CTR schemes.

If you need extra support, you may be able to receive a one‑off or ongoing payment paid to your Council Tax account from the Exceptional Hardship Fund made under S13A (1)(a) of the 1992 Act (also known as discretionary help).

To be considered for a discretionary payment from the Exceptional Hardship Fund, you should normally already be receiving, or have applied for, Council Tax Reduction (CTR).

In exceptional circumstances, we may make a discretionary payment even if you do not qualify for CTR.

You will need to provide evidence when you apply: Apply for discretionary help.

Additional support available

Other information and schemes which can help pay other bills can be found on:

If you have applied for Council Tax Reduction and discretionary help but do not qualify, or you still cannot afford to pay your Council Tax, you can apply for support under a Section 13A(1)(c) request.

To be considered for Section 13A(1)(c) support, you must show that you are vulnerable and experiencing significant financial hardship.

To apply, email the Council Tax team at [email protected] with:

- details of your circumstances and why you need additional support

- a completed income and expenditure form:

- relevant evidence to support your request, such as bank statements, medical information, or proof of debts

You must tell us within 21 days if:

- your income changes

- your household changes

- you move home

- you stop receiving a qualifying benefit

View policies for:

- CTR Working Age Scheme (PDF, 678 KB)

- Council Tax Reduction discretionary award policy (PDF, 180 KB)

- Council Tax discretionary discount policy (PDF, 250 KB)